0330 127 2333

0330 127 2333

The …

Comprehensive Insurance Guide for Lighting Systems Manufacturers

Safeguarding Your Innovative Manufacturing Business from Concept to Completion

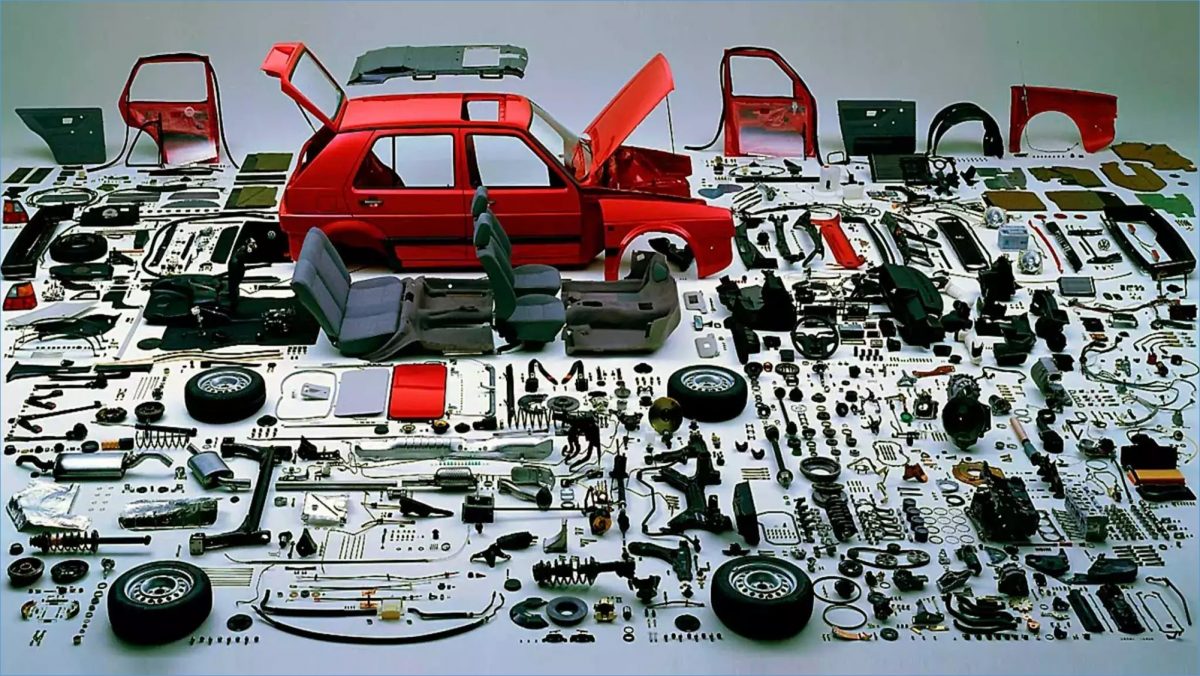

Specialist insurance coverage designed for automotive component manufacturing, protecting against product liability, equipment breakdown, supply chain disruption, and regulatory compliance risks.

Our specialist automotive component manufacturing insurance provides complete protection for your manufacturing operations, from raw materials to finished products delivered to automotive OEMs and aftermarket suppliers.

Automotive component manufacturing faces unique challenges that require specialist insurance expertise:

Our automotive component manufacturing insurance addresses key regulatory and compliance requirements:

Insure24 understood our complex supply chain risks and provided coverage that actually protects our business. Their claims team responded within hours when we had a production line fire.

Manufacturing Director, Tier 1 Brake Component SupplierDon't leave your automotive component manufacturing exposed to unnecessary risks.

Our specialist team will assess your venue's unique needs and provide a comprehensive insurance solution that protects your business, your customers, and your livelihood.

Call us now: 0330 127 2333

Or get an instant online quote at insure24.co.uk

What types of automotive component manufacturing do you insure?

We provide insurance for all types of automotive component manufacturing, including engine components, transmission parts, brake systems, electrical components, interior/exterior parts, safety systems, and aftermarket suppliers. Coverage is available for tier 1, tier 2, and tier 3 suppliers.

How much product liability coverage do I need?

Product liability limits typically range from £1M to £50M+ depending on your component type, customer requirements, and market exposure. Safety-critical components often require higher limits. We'll assess your specific needs based on your products and contracts.

Does the insurance cover international sales?

Yes, our product liability coverage includes worldwide territorial limits for components exported internationally. We can also arrange coverage for overseas manufacturing facilities, joint ventures, and distribution agreements.

What happens if my components cause a vehicle recall?

Our product liability coverage includes recall expenses, investigation costs, and third-party claims arising from defective components. We work with specialist recall consultants to minimize costs and manage the process effectively.

Is cyber insurance really necessary for manufacturing?

Absolutely. Modern manufacturing relies heavily on connected systems, CAD/CAM software, and customer data exchange. Cyber attacks can shut down production lines, steal intellectual property, and compromise customer information. Coverage is essential.

How quickly can you arrange coverage?

For standard manufacturing operations, we can often provide quotes within 24-48 hours and arrange coverage within a week. Complex operations or high-risk exposures may require additional underwriting time.

What information do you need for a quote?

We'll need details about your manufacturing processes, annual turnover, product types, customer base, quality certifications, claims history, and current insurance arrangements. A site visit may be required for larger operations.

Can you cover prototype and development work?

Yes, our professional indemnity coverage includes design and development activities, prototype testing, and pre-production services. We understand the unique risks of R&D operations in automotive component development.

What about coverage for contract manufacturing?

We provide specialized coverage for contract manufacturing, including protection for customer-owned tooling, materials, and intellectual property. Coverage can be tailored to your specific contractual obligations and liability exposures.

How does business interruption coverage work?

Business interruption coverage compensates for lost revenue and ongoing expenses when production is halted due to insured events. This includes coverage for supply chain disruption, customer penalty clauses, and additional costs to minimize the interruption period.

Are there discounts for good safety records?

Yes, manufacturing with strong safety records, quality certifications (ISO/TS 16949), and robust risk management systems often qualify for premium discounts. We reward proactive risk management and continuous improvement initiatives.

What's not covered by standard policies?

Standard exclusions typically include wear and tear, design defects (unless PI coverage is included), war and terrorism, nuclear risks, and pollution (unless specifically covered). We'll explain all exclusions and available extensions during the quotation process.

Can you help with risk management?

Yes, we provide access to risk management consultants who specialize in manufacturing operations. Services include safety audits, quality system reviews, supply chain risk assessments, and loss prevention recommendations.

How do claims work in practice?

Our 24/7 claims service ensures rapid response to incidents. We assign specialist adjusters familiar with manufacturing operations and work to minimize business disruption while ensuring fair and prompt settlement of valid claims.

What about environmental liability?

Environmental liability coverage can be included to protect against pollution incidents, contamination cleanup costs, and regulatory fines. This is particularly important for manufacturing using chemicals, coatings, or other potentially hazardous materials.

Do you cover electric vehicle component manufacturing?

Yes, we have specialist expertise in EV component manufacturing risks, including battery systems, charging components, power electronics, and software integration. Coverage addresses the unique risks of this rapidly evolving sector.

How often should I review my coverage?

We recommend annual policy reviews to ensure coverage keeps pace with business growth, new products, changing regulations, and evolving risks. Major changes like new facilities, acquisitions, or product launches should trigger immediate reviews.

What makes automotive component insurance different?

Automotive component manufacturing has unique characteristics: strict quality requirements, just-in-time delivery pressures, long product lifecycles, safety-critical applications, and complex supply chains. Standard manufacturing insurance often doesn't address these specialized risks adequately.

Can you cover both OEM and aftermarket suppliers?

Yes, we provide coverage for both original equipment manufacturing and aftermarket suppliers. Each market has different risk profiles and requirements, which we address through tailored coverage solutions.

What about coverage for autonomous vehicle components?

We stay ahead of emerging technologies and provide coverage for manufacturing of autonomous vehicle components, including sensors, software, and control systems. This includes product liability and professional indemnity for these cutting-edge technologies.

How do you handle multi-site manufacturing?

We can arrange comprehensive coverage for multi-site operations under a single master policy, providing consistent coverage terms while addressing site-specific risks. This approach often provides cost efficiencies and simplified administration.

What support do you provide during claims?

Our claims support includes immediate incident response, specialist loss adjusters, technical experts, legal support where needed, and regular communication throughout the claims process. We aim to minimize disruption and expedite resolution.

What is the average cost of automotive component manufacturing insurance?

Insurance costs vary significantly based on component type, annual turnover, and risk exposure. Small manufacturing may pay £2,000-£5,000 annually, while large tier 1 suppliers can pay £50,000+ for comprehensive coverage including high product liability limits and worldwide protection.

Do I need separate insurance for engine component manufacturing?

Engine components are safety-critical parts requiring specialized coverage with higher product liability limits. Standard manufacturing insurance may not provide adequate protection for engine-related recalls or failures. We recommend dedicated automotive component coverage with engine-specific endorsements.

How does insurance work for brake system manufacturing?

Brake system manufacturing face the highest product liability risks in automotive manufacturing. Coverage must include recall expenses, third-party injury claims, and regulatory defense costs. Minimum coverage typically starts at £10M with many requiring £25M+ limits for OEM contracts.

What insurance do electrical component manufacturing need?

Electrical component manufacturing need product liability for system failures, cyber insurance for connected components, and professional indemnity for software/firmware development. Coverage should address electromagnetic interference, fire risks, and autonomous vehicle integration issues.

Is insurance different for safety-critical automotive components?

Yes, safety-critical components like airbags, braking systems, and steering components require enhanced coverage with higher limits, stricter underwriting, and specialized recall protection. Insurers assess manufacturing quality systems, testing protocols, and regulatory compliance more rigorously.

What coverage do transmission component manufacturing need?

Transmission manufacturing need comprehensive product liability for mechanical failures, business interruption for production delays, and professional indemnity for design services. Coverage should include warranty claims, customer penalty costs, and supply chain disruption protection.

How much does product liability insurance cost for automotive parts?

Product liability premiums range from 0.1% to 2% of annual turnover depending on component risk level. Safety-critical parts command higher rates, while interior trim components are typically lower risk. Factors include claims history, quality certifications, and customer base.

Do aftermarket automotive parts manufacturing need different insurance?

Aftermarket manufacturing often face different risks including counterfeit concerns, varied quality standards, and diverse distribution channels. Insurance should address these unique exposures while providing competitive coverage for non-OEM market requirements.

What insurance do automotive plastic component manufacturing need?

Plastic component manufacturing need coverage for material defects, environmental liability from chemical processes, fire risks from manufacturing, and product liability for component failures. Coverage should include mold/tooling protection and contamination risks.

How does ISO/TS 16949 certification affect insurance premiums?

ISO/TS 16949 certification typically reduces insurance premiums by 10-25% as it demonstrates robust quality management systems. Insurers view certified manufacturing as lower risk due to systematic defect prevention and continuous improvement processes.

What insurance do automotive metal stamping companies need?

Metal stamping operations need coverage for press equipment, tooling and dies, employee injury from heavy machinery, and product liability for dimensional defects. Business interruption coverage is crucial due to high fixed costs and customer delivery requirements.

Do automotive component exporters need special insurance?

Yes, exporters need worldwide product liability coverage, marine cargo insurance for shipments, and foreign regulatory compliance protection. Coverage should address different legal systems, currency fluctuations, and international recall coordination.

What insurance covers automotive component testing and validation?

Professional indemnity insurance covers testing errors, validation mistakes, and certification issues. Coverage includes costs of re-testing, customer delays, and liability for incorrect test results that lead to product failures or recalls.

How does insurance work for automotive component joint ventures?

Joint ventures require careful coordination of insurance coverage between partners. Policies must address shared liabilities, intellectual property protection, and operational control issues. Master policies can provide consistent coverage across all venture participants.

What insurance do automotive fastener manufacturing need?

Fastener manufacturing need product liability for mechanical failures, recall coverage for safety-critical applications, and business interruption for high-volume production. Coverage should address material defects, coating failures, and dimensional tolerance issues.

Do automotive component manufacturing need directors and officers insurance?

D&O insurance is essential for incorporated manufacturing, protecting directors from personal liability in product recall situations, regulatory investigations, and shareholder claims. Coverage is particularly important for publicly traded component suppliers.

What insurance covers automotive component supply chain disruption?

Supply chain disruption coverage extends business interruption insurance to include supplier failures, raw material shortages, and logistics interruptions. This is crucial for just-in-time manufacturing environments where delays have immediate financial impact.

How does insurance work for automotive component research and development?

R&D activities require professional indemnity for design errors, intellectual property insurance for patent disputes, and product liability for prototype testing. Coverage should address the unique risks of developing next-generation automotive technologies.

What insurance do automotive bearing manufacturing need?

Bearing manufacturing need comprehensive product liability for mechanical failures, precision equipment coverage for manufacturing machinery, and business interruption for production delays. Coverage should address lubrication failures, material defects, and precision tolerance issues.

Do automotive component manufacturing need employment practices liability insurance?

EPLI protects against wrongful termination, discrimination, and harassment claims from employees. This is increasingly important for manufacturing facing skilled labor shortages and diverse workforce management challenges in the automotive industry.

What insurance covers automotive component warranty claims?

Extended warranty insurance can cover manufacturer warranty obligations beyond standard policy periods. This is particularly valuable for components with long service lives or when customer contracts require extended warranty periods.

How does insurance work for automotive component manufacturing in Wales?

Welsh manufacturing benefit from local expertise understanding regional business conditions, Welsh government incentives, and proximity to major automotive plants. Coverage addresses specific risks like weather-related disruptions and transport logistics in Wales.

Safeguarding Your Innovative Manufacturing Business from Concept to Completion

Wiring harness manufacturing is a…

In the rapidly evolving landscape of auto…

The electrical and elec…

In the complex and precision-driven world of m…

The exhaust systems manufacturing in…

The fuel system co…

Transmission systems ma…

The engi…

The …